Introduction

When raising capital through private placements, most issuers rely on Rule 506 of Regulation D under the Securities Act of 1933. This powerful exemption allows companies to raise unlimited capital without SEC registration, but it comes in two distinct flavors: Rule 506(b) and Rule 506(c). Each has unique advantages and limitations that can significantly impact your fundraising strategy.

Understanding these differences is crucial. Choose correctly, and you’ll have a smooth, compliant capital raise. Choose incorrectly, and you may find yourself limited in how you can market your offering or burdened with expensive verification requirements.

The Foundation: What Both Rules Share

Before diving into the differences, it’s important to understand what Rule 506(b) and Rule 506(c) have in common:

- Unlimited capital raising: No cap on the amount you can raise

- Federal preemption: Both preempt state securities registration (though states may require notice filings and fees)

- SEC filing requirements: Form D must be filed within 15 days of the first sale

- Bad actor disqualification: Neither exemption is available to issuers subject to “bad actor” provisions

- Safe harbor status: Both provide safe harbor under Section 4(a)(2) of the Securities Act

Rule 506(b): The Traditional Approach

Overview

Rule 506(b) has been the workhorse of private placements since 1982. It remains the most popular choice, particularly for funds with established networks and those who value flexibility in their investor base.

Key Features

Investor Composition:

- Unlimited accredited investors

- Up to 35 non-accredited but sophisticated investors

- No verification requirement for accredited investor status

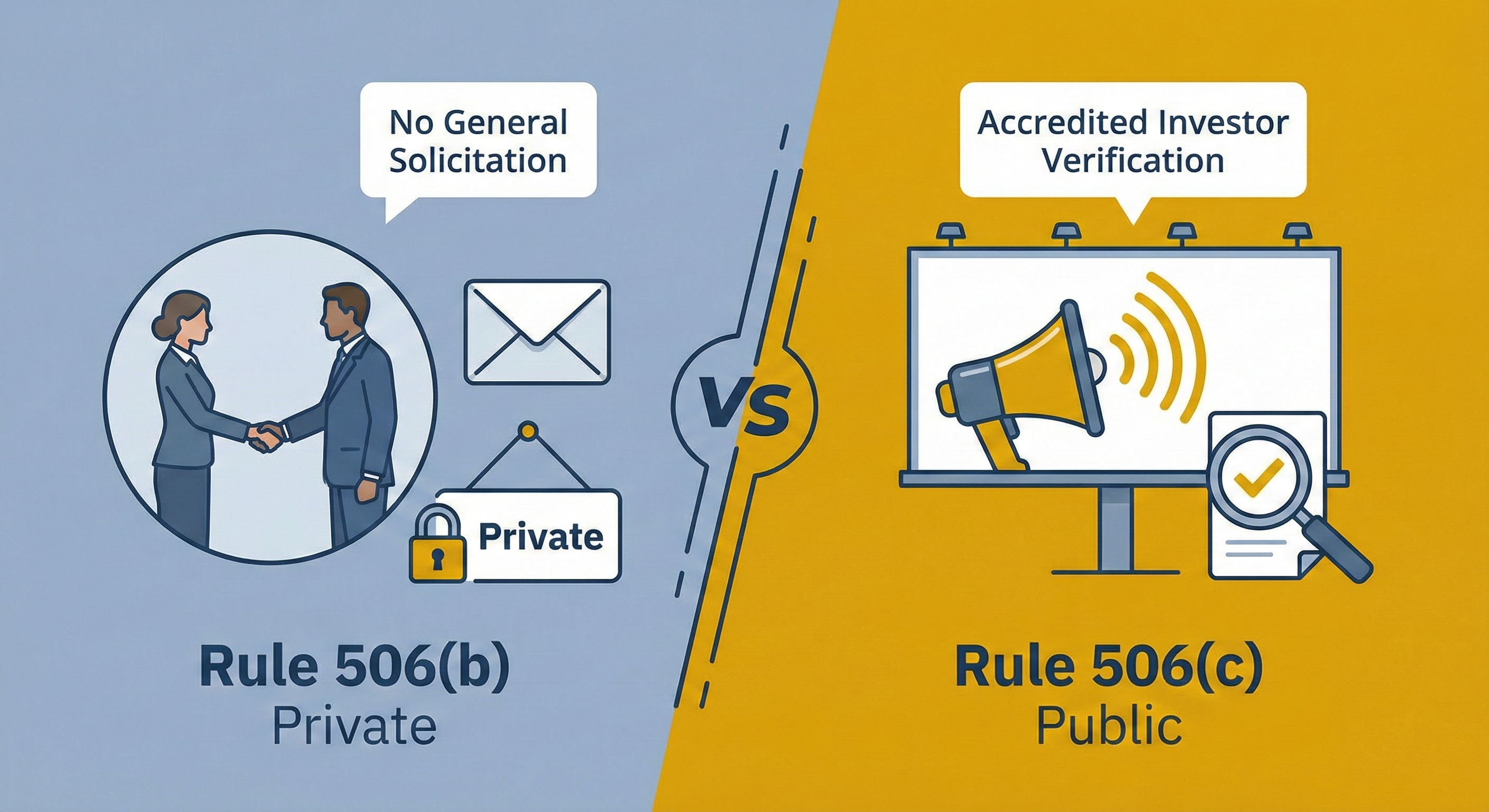

Marketing Restrictions:

- No general solicitation or advertising permitted

- Must have “substantive pre-existing relationship” with investors

- Cannot publicly market the offering

Advantages of Rule 506(b)

- Flexibility in investor qualification: Self-certification of accredited status is sufficient

- Established precedent: Decades of market practice and legal guidance

- Lower compliance costs: No expensive verification procedures required

- Non-accredited investor option: Ability to include up to 35 sophisticated investors

Disadvantages of Rule 506(b)

- Marketing limitations: Cannot use public advertising, websites, or social media to attract investors

- Network dependency: Success depends on existing relationships and warm introductions

- Disclosure burden: If non-accredited investors participate, extensive disclosure requirements apply

- Relationship building: Must establish qualifying relationships before making any offer

Practical Considerations for Rule 506(b)

For Fund Managers:

- Most funds rely exclusively on accredited investors to avoid disclosure complexities

- Non-accredited investors can prevent a fund from qualifying as an accredited investor itself

- The pre-existing relationship requirement demands careful compliance documentation

Best Suited For:

- Established managers with strong networks

- Funds targeting institutional investors

- Offerings where investor privacy is paramount

- Situations where verification costs would be prohibitive

Rule 506(c): The Modern Alternative

Overview

Added in 2013 as part of the JOBS Act, Rule 506(c) revolutionized private placements by permitting general solicitation—but with a significant catch: mandatory verification of accredited investor status.

Key Features

Investor Composition:

- Unlimited accredited investors only

- No non-accredited investors permitted

- Mandatory verification of accredited status

Marketing Freedom:

- General solicitation and advertising permitted

- Can use websites, social media, and public events

- No pre-existing relationship requirement

Advantages of Rule 506(c)

- Marketing flexibility: Use any channel to reach potential investors

- Broader reach: Access investors beyond your immediate network

- Scalability: Easier to build systematic fundraising processes

- Transparency: Can publicly discuss investment opportunities

Disadvantages of Rule 506(c)

- Verification burden: Must take “reasonable steps” to verify accredited status

- Higher costs: Verification procedures add time and expense

- Investor friction: Verification requirements may deter some investors

- No non-accredited option: Cannot include sophisticated but non-accredited investors

Verification Requirements: The Devil in the Details

The SEC provides several safe harbor methods for verification:

Income Verification:

- Review tax documents for two most recent years

- Obtain written representation of current year expectations

- Documents: W-2s, 1099s, tax returns, K-1s

Net Worth Verification:

- Review assets: Bank statements, brokerage statements, property appraisals

- Review liabilities: Credit reports dated within 90 days

- Exclude primary residence value and associated debt

Third-Party Verification:

- Written confirmation from registered broker-dealer, SEC-registered investment adviser, licensed attorney, or certified public accountant

- Must confirm verification within prior three months

Previous Investor Verification:

- For repeat investors, can rely on previous verification if still valid

- Must obtain written representation that status hasn’t changed

Making the Choice: Key Decision Factors

Choose Rule 506(b) When:

- You have strong existing networks: Your investors come through relationships and warm introductions

- Verification creates friction: Your target investors value privacy or find verification burdensome

- You need flexibility: You want the option to include sophisticated non-accredited investors

- Marketing isn’t critical: You don’t need public advertising to reach your target audience

Choose Rule 506(c) When:

- You need marketing freedom: Success depends on reaching new investors through public channels

- You’re building a platform: Systematic, scalable fundraising is your goal

- Your investors expect it: Many institutional investors are comfortable with verification

- You want transparency: Public discussion of your offering is valuable

Common Pitfalls and How to Avoid Them

Rule 506(b) Pitfalls:

- Inadvertent general solicitation: Even casual public mentions can disqualify the exemption

- Weak relationship documentation: Failing to document pre-existing relationships

- Non-accredited investor issues: Underestimating disclosure obligations

Rule 506(c) Pitfalls:

- Insufficient verification: Self-certification is never enough under Rule 506(c)

- Poor marketing execution: General solicitation doesn’t guarantee effective marketing

- Verification delays: Not building enough time into the closing process

Special Considerations for Investment Funds

Fund-Specific Issues:

- Investor count limitations: Consider Investment Company Act implications (3(c)(1) vs. 3(c)(7))

- ERISA considerations: Plan asset rules may affect your choice

- Side letter negotiations: Verification requirements may complicate custom terms

- Feeder fund structures: Consider how the exemption choice affects master-feeder arrangements

Hybrid Approaches:

Some funds use both exemptions strategically:

- Initial close under Rule 506(b) with known investors

- Subsequent closings under Rule 506(c) for broader marketing

- Separate feeder funds using different exemptions

Conclusion

The choice between Rule 506(b) and Rule 506(c) isn’t just a technical compliance decision—it’s a strategic choice that shapes your entire fundraising approach. Rule 506(b) offers flexibility and established practices but limits your marketing reach. Rule 506(c) provides marketing freedom but requires rigorous verification procedures.

For most established fund managers with strong networks, Rule 506(b) remains the preferred choice. However, emerging managers, fintech platforms, and those seeking to democratize access to private investments increasingly turn to Rule 506(c).

The key is matching the exemption to your specific circumstances: your investor base, marketing needs, compliance resources, and strategic goals. There’s no universally correct answer—only the right answer for your particular situation.

Note: This article provides general information only and does not constitute legal advice. The rules discussed are subject to various limitations not covered here, including restrictions under the Exchange Act Section 12(g) and Investment Company Act Section 3(c). Always consult with qualified securities counsel before conducting any securities offering.

Related BlackHill Law Services:

- Raise Ready Package — Capital raising legal support from $5,997

- Form D Filing — SEC Form D filing from $1,995

- Securities Practice Area