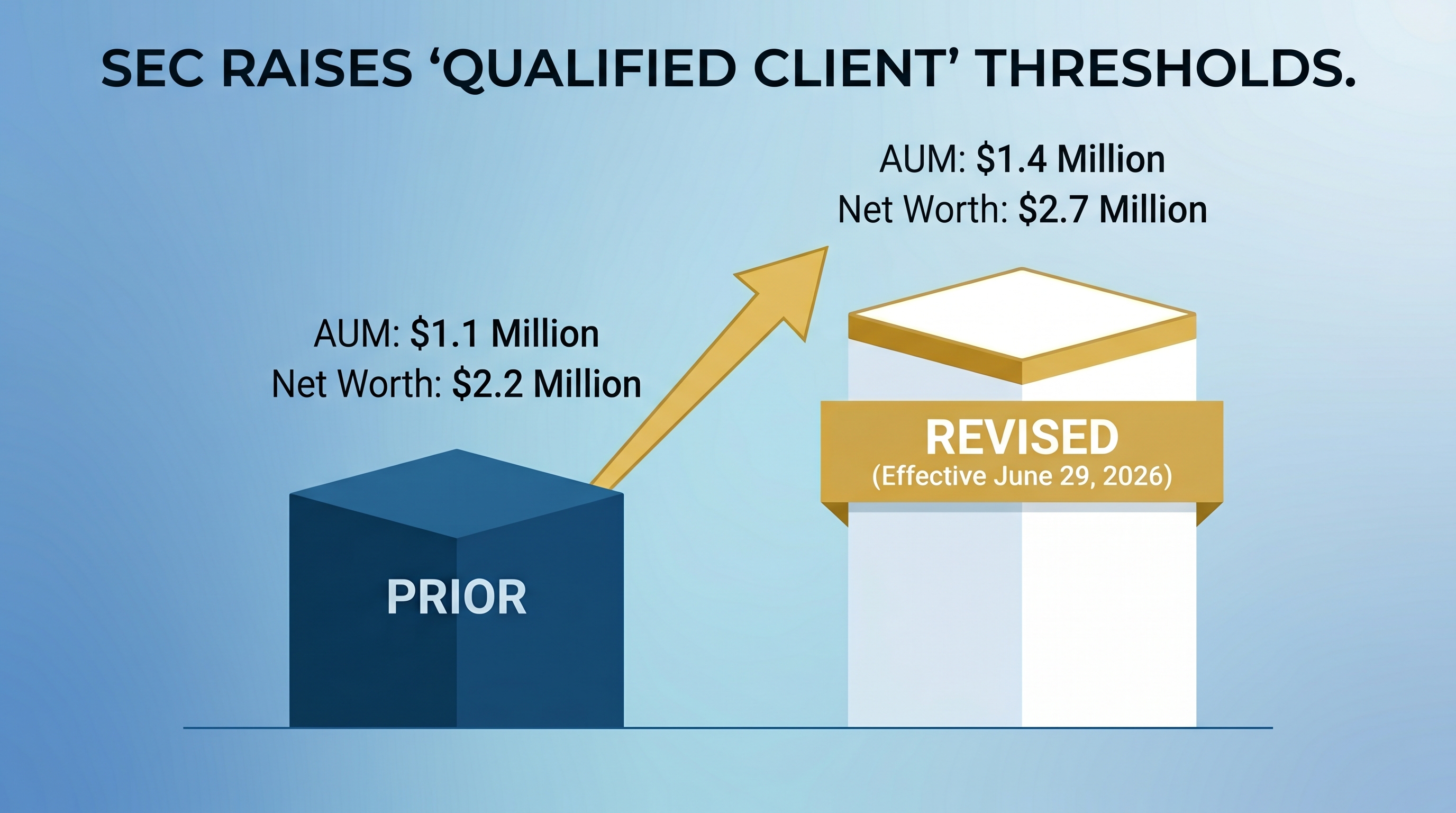

The new numbers at a glance

The adjustment is a routine inflation update that the SEC is required to make every five years under Section 418 of the Dodd-Frank Act, based on the Consumer Price Index. It is not a policy shift. But the dollar figures baked into your subscription documents, advisory agreements, and compliance manual will soon be out of date.

| Test | Through June 28, 2026 | Effective June 29, 2026 |

|---|---|---|

| Assets under management with the adviser | $1,100,000 | $1,400,000 |

| Net worth | $2,200,000 | $2,700,000 |

The net worth test is measured at the time the person enters into the advisory arrangement, may include assets held jointly with a spouse, and excludes the value of the person’s primary residence and related debt.

Refresher: why “qualified client” matters

Section 205(a)(1) of the Advisers Act generally prohibits an SEC-registered adviser from charging a client performance-based compensation, which means a fee or allocation tied to capital gains or capital appreciation. Rule 205-3 is the exemption: you may charge performance compensation, but only to a client who is a qualified client.

A private fund’s carried interest is treated as performance compensation, so each investor admitted to the fund generally has to meet the qualified client standard. The same is true for a separately managed account with a performance fee.

If you charge a performance fee or carry to someone who is not a qualified client, the arrangement violates Section 205, which can mean fee disgorgement, rescission rights for the investor, and an examination finding you do not want on your record.

Grandfathering

The new thresholds are not retroactive.

- Existing investors and clients are fine. If a person was already a party to your advisory agreement (or already admitted to your fund) before June 29, 2026, they can continue to rely on the dollar amounts that applied when they signed. You do not have to re-qualify them.

- New parties on or after June 29, 2026 must meet the new, higher thresholds. If someone becomes a party to an advisory agreement on or after the effective date, they need at least $1,400,000 under management with you or a $2,700,000 net worth.

For fund managers, the line that matters is when an investor is admitted to the fund. A new investor who subscribes at a closing on or after June 29, 2026 must satisfy the new thresholds, even if the fund itself launched years earlier.

Action item 1: Update fund documents for any active deals

Any deal, fund, or account that is still open and admitting investors on or after June 29, 2026 should be papered to the new numbers before your next closing. Review and update:

- Subscription agreements and investor questionnaires. The qualified client representation almost always recites the specific dollar figures. Update them to $1,400,000 and $2,700,000.

- Separately managed account and advisory agreements that carry a performance fee.

- Side letters that restate eligibility representations.

If you have an active raise or a deal closing this summer, do not let a new investor sign the old, lower-threshold documents on or after the effective date.

Action item 2: Update your internal compliance policies and processes

The numbers also live inside your compliance program, not just your investor-facing documents. Before June 29, 2026, update:

- Your compliance manual and written policies wherever the qualified client thresholds are stated.

- Your subscription review and investor onboarding checklists, so the person verifying eligibility is testing against $1,400,000 and $2,700,000.

- Any intake forms, CRM fields, or templates that capture qualified client status.

- Your team. Make sure whoever reviews subscriptions and signs off on new investors knows the thresholds changed and when.

Then document the change. A short memo to file noting that you reviewed and updated the thresholds as of the effective date is exactly the kind of record an examiner expects to see.

What you do not need to do

You do not need to claw back, re-paper, or re-qualify investors who were already in the fund or already under contract before June 29, 2026.

A note for state-registered and exempt advisers

Rule 205-3 governs SEC-registered advisers. If you are a state-registered adviser, your state’s performance-fee rule often mirrors the federal qualified client standard, but you should confirm the figures your state uses. If you are an exempt reporting adviser, the Section 205 performance-fee restriction generally does not apply to you in the same way, but the qualified client standard frequently shows up in fund documents anyway, so it is still worth aligning your subscription package with the current numbers.

If you want a second set of eyes on your subscription documents or your compliance manual before the deadline, reach out. We can turn a document review around quickly.